This is the next post in Plan Proponent’s series on the confirmation-related recommendations in the ABI Commission Report (and, in particular, its Exiting the Case piece). We introduced the Commission’s “Redemption Option Value” (“ROV”) recommendation in our prior post. We’ll wrap-up the ROV discussion in this post by discussingthe ROV calculation itself.

In preparing this post, I reviewed our prior post. Only then did I realize that we could not have introduced such an arguably radical recommendation in a more nondescript fashion. Such is the risk of these “book report”-style posts (i.e., “First the Commission said this, and then it recommended this, etc.”). So, let’s take a step back and let the ROV recommendation sink-in.

On the one hand, the Commission’s justification for ROV (which we discussed previously) makes sense and even sounds noble. Prof. Michelle Harner (the Commission’s Reporter) sums it up: “This concept is intended to mitigate valuation fluctuations caused by the timing of a valuation-realization event in chapter 11.”

On the other hand, ROV represents a significant departure from the Code (and the absolute priority rule, in particular). In plain English, the Commission is recommending that, in certain circumstances, senior creditors should be required to distribute some of the value of their collateral (the ROV) to “out-of-the-money” constituencies, even if such senior creditors are not being paid in full themselves.

For some, that’s a radical idea. See the list of criticisms and concerns, and related article links, below. And not only is the ROV recommendation a significant departure from current practice, but it’s also rather complex–some might say, a valuation expert’s dream come true. Specifically, the Commission concluded that “using a market-based method such as the Black-Scholes model purely as a working formula would likely be the best way to consistently and accurately determine the value of the hypothetical redemption option.” In a word, “yikes”!

[I first encountered Black-Scholes in a “Derivative Security Markets” class as a Finance major at the University of Georgia in ’98. And the only thing I remember about that class is that some Wall Street firm had recently paid the professor a boat load of money to home grow its option pricing software. This isn’t for the feint of heart!]

Generally, the Black-Scholes Model values options based on 4 factors:

- Strike price of the option

- Term of the option

- Volatility

- Risk-free rate

The Commission explains each factor as it relates ROV, as follows.

The “strike price” is 100% of the redemption price. The redemption price is the full face amount of the senior debt, including any deficiency claim (without considering bifurcation), interest at the non-default contract rate, and allowable fees and expenses through the hypothetical option exercise date. The term of the option is assumed to be the 3 year period after the petition date. The volatility factor can be determined by looking at the historical volatility of similar companies (or agreeing on a set metric, such as the “average 60 day forward volatility of the S&P 500 Index for the past 4 years”). In turn, the risk-free rate can be the U.S. Treasury rate.

In particular, the option term factor came about from the Commission’s conclusion that most economic cycles, industry events, operational issues, etc. that cause timing issues to impact value allocation tend to resolve themselves within 3 to 5 years. Although some Commissioners pushed for a 5 year term, the Commission concluded that, on the whole and given the average duration of Chapter 11 cases, a 3 year option should sufficiently remedy the value allocation issues that motivated the ROV recommendation.

The Commission then provides a limited example, with the following assumptions:

- Senior class is entitled to 100% of the firm value

- Effective Date of plan = 1 year after petition date (i.e., a 2 year term)

- Risk-free rate of 2.23%

The Commission then just ran the inputs through the following formula, and out popped the ROV:

(That’s a joke. The above picture may not even be the Black-Scholes formula. Google Images says it is, at least.)

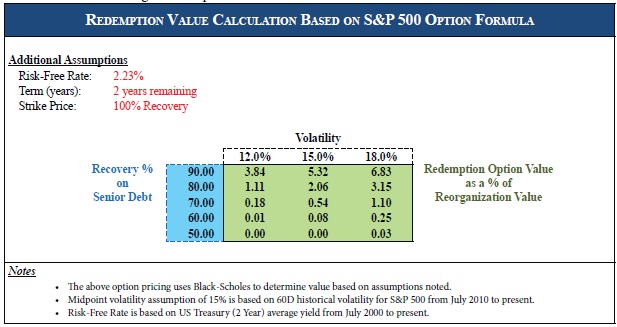

For our discussion, we’ll just have to accept the Black-Scholes part of the calculation as delivered. However, the Commission does provide the following graphic to illustrate the impact of the senior debt’s expected recovery and the assumed volatility on the ROV (as a % of reorganization value):

For example, at a 50% recovery, and almost regardless of volatility, the ROV as a percentage of reorganization value is basically 0%. However, at a 90% recovery, the ROV ranges from 3.84% to 6.83% for the given volatility assumptions. Under the ROV recommendation, those percentages would be distributed to the immediately junior class as cash, debt, stock, or the like (not as an actual option).

[Black-Scholes is not the only contemplated methodology. In fact, it could be inappropriate or another model (e.g., the “Binomial Options Pricing Model,” a “Monte Carlo” options model, etc.) could be more appropriate.]

Generally, the closer the senior class is to being fully-paid, the more likely it is that there will be an ROV entitlement (and vice versa). ROV for a 50% recovery (or less) would be unusual. Mathematically, relatively shorter cases in relatively volatile markets should produce the most ROV. And that makes sense given that concerns about those sorts of cases drove the ROV recommendation in the first place.

[We won’t dwell on the slight differences, but the ROV calculation would be made for Section 363 sales too.]

That’s about as detailed as we can get without engaging an expert.

Therefore, we’ll conclude by identifying some of the concerns and criticisms that we gleaned from other articles:

- The ROV concept (of “relative priority”?) is a significant departure from the absolute priority rule;

- ROV imposes an inappropriate “tax” or “surcharge” on senior secured creditors;

- Given the attendant complexity, cases could actually take longer and become more expensive;

- ROV could have a significant impact on “broader credit markets”;

- There is no definitive ROV methodology, such that judicial valuation will become even murkier;

- The procedural elements are unclear regarding objections, etc.;

- Empirical data justifying ROV is not available (or, at least, was not presented).

The following articles address some of the above criticisms and concerns more extensively:

Redemption Option Value: Broad Implications for Secured Lenders (by Chapman and Cutler, LLP)

(This article is quite critical, but it’s also thoughtful; the Report needs to be challenged and questioned.)

(This article addresses concerns, but it’s also useful as an easy-to-follow Q&A.)

Additionally, Prof. Harner addressed ROV (and addressed some of the criticisms) here:

Chapter 11 Reform: Refining the Tools Available to Rehabilitate Distressed Businesses

That should cover Redemption Option Value for the moment. However, we know some super-smart valuation folks who we’re going to try and tackle for their input on ROV–particularly as it relates to the ROV calculation.

In our next post, we’ll continue with Part C.2 (“New Value Corollary”). Stay tuned.