This is the next post in Plan Proponent’s series on the confirmation-related recommendations in the ABI Commission Report (and, in particular, its Exiting the Case piece). Part B of the “Exiting the Case” piece is titled “Approval of Section 363x Sales.”

Acknowledging various concerns raised by courts about Section 363 sales, the Commission considered the extent to which Section 363 sales should be subject to the rigors of the plan process. Although Part B is most notable for the Commission’s recommendations (listed below), the background provided by the Commission about Section 363 issues is also useful.

First, Part B is just one of many sections of the Report addressing the sale of all or substantially all of a debtor’s assets under Section 363(b) of the Code.

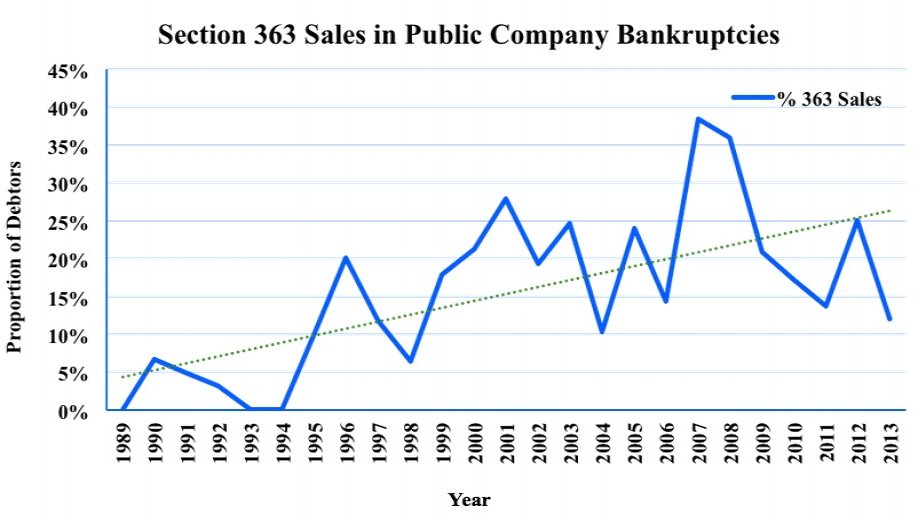

Second, the Commission attempts to introduce empirical data regarding 363 sales in Chapter 11. However, it warns that such data is limited, mixed, and difficult to interpret. Not only is it difficult to “code” the data as reflecting a “liquidation, going concern sale (i.e., section 363x sale), or confirmed plan,” but it is also difficult to “collect and code creditors’ recoveries.” In fact, the Commission suggests that much of the data is from large Chapter 11 cases, only (i.e., cases involving assets of $100 million or more). Finally, the Commission warns that dockets and, thus, the data, rarely reflect the unique dynamics that drive a particular case. With those caveats in mind, the Commission supplied the following chart:

Third, the Commission identifies the concerns that some courts have raised regarding Section 363 sales, particularly those sales that involve a sale of all or substantially all of a debtor’s assets:

Third, the Commission identifies the concerns that some courts have raised regarding Section 363 sales, particularly those sales that involve a sale of all or substantially all of a debtor’s assets:

- Potential avoidance of notice and due process;

- Pursuit of a fast-track process before parties-in-interest can obtain adequate information;

- Insufficient time for parties-in-interest to identify restructuring alternatives;

- Determination of ultimate creditor distributions without voting and other plan protections;

- Sale timing issues that can impact, if not chill, asset values and, thus, diminish recoveries; and

- Additional potential impacts on asset values due to abbreviated marketing periods.

Fourth, and in light of the above concerns, the Commission considered the extent to which a sale of all or substantially all of a debtor’s assets is tantamount to a reorganization. After all, such sales can result in a change in control, result in final creditor distributions, and position the debtor to continue in business in another form. The Commission concluded that such sales justify incorporating some of the plan protections under Section 1129. See below.

[The above concerns often come to a head in cases addressing whether a 363 sale is, in fact, a “sub rosa” (de facto) plan. See, e.g., In re Gen. Motors Corp., 407 B.R. 463 (Bankr. S.D.N.Y. 2009). Steve Jakubowski had a good post about 363 sales and sub rosa plans on his Bankruptcy Litigation Blog. See also Reginald Jackson’s 2010 article for the Southeastern Bankruptcy Law Institute (the pride and joy of the Georgia Bankruptcy Bar.)]

Fifth, the Commission emphasized how the typical standard of review for a Section 363 sale differs from the standard of review applied to a plan under Section 1129. The typical standard of review for a 363 sale is a business judgment rule approach, which looks for a good business reason for the sale and might impose some heightened scrutiny. Arguably, the standard for plans is much stricter, and demands a vote, good faith, satisfaction of the best interests of creditors test under 1129(a)(7), payment of certain administrative claims, no unfair discrimination, and “fair and equitable” treatment of dissenting creditors.

Ultimately, the Commission concluded that the 363 sale process should protect creditors in the same way that the 1129 plan process protects creditors.

With that in mind, the Commission made the following Recommendations for Section 363 sales:

- Sale should be in the best interests of the estate by a preponderance of the evidence;

- Sale should comply with provisions that are comparable to the 1129 plan requirements;

- Sale and sale proponent should comply with the applicable provisions of the Code;

- Sale should be proposed in good faith and not by any means forbidden by law;

- Sale-related costs and expenses should be reasonable;

- Administrative-type claims (through the sale date) should be paid/resolved;

- Statutory bankruptcy fees should be paid at or before closing;

- There should be adequate notice and an opportunity to be heard by all parties-in-interest impacted by proposed purchaser protections.

Additionally, the Commission incorporates its 363-related recommendations from other parts of the Report, including:

- Section VI.G (Orders Resolving Chapter 11 Case – Exit Orders) (we’ll cover that separately in our series)

- Section IV.C.2 (Timing of Section 363x Sales) (recommending a 60 day sale moratorium)

- Section V.B (Use, Sale, or Lease of Property of the Estate) (i.e., non-ordinary course transactions)

In our next post on the ABI Commission Report, we will address the first portion of Part C (“Value Determinations, Allocation, and Distributions”).